SWIFT MT – Serial and Cover Method

This is one of the most important articles from SWIFT payments’ perspective and it is critical that you fully understand the concepts laid out here.

Payments are cleared and settled via 2 primary methods:

- Through a payment market infrastructure (PMI)

- Through correspondent banking

Through payment market infrastructure:

This is the case where bank A and bank B are direct participants of this PMI aka CSM. IN General usage the concept of serial and cover does not apply here but if you put a gun to my head, I would say is very close to the serial method.

Through correspondent banking:

This is the case where banks open accounts with each other (Nostro/Vostro) and settle funds directly. The prerequisite here is that banks need to open accounts with each other or in other words they need to have an accounting relationship with the other bank.

Now, let us try to understand the connection between sending/receiving SWIFT messages and the movement of funds from one party to another during the entire payment chain.

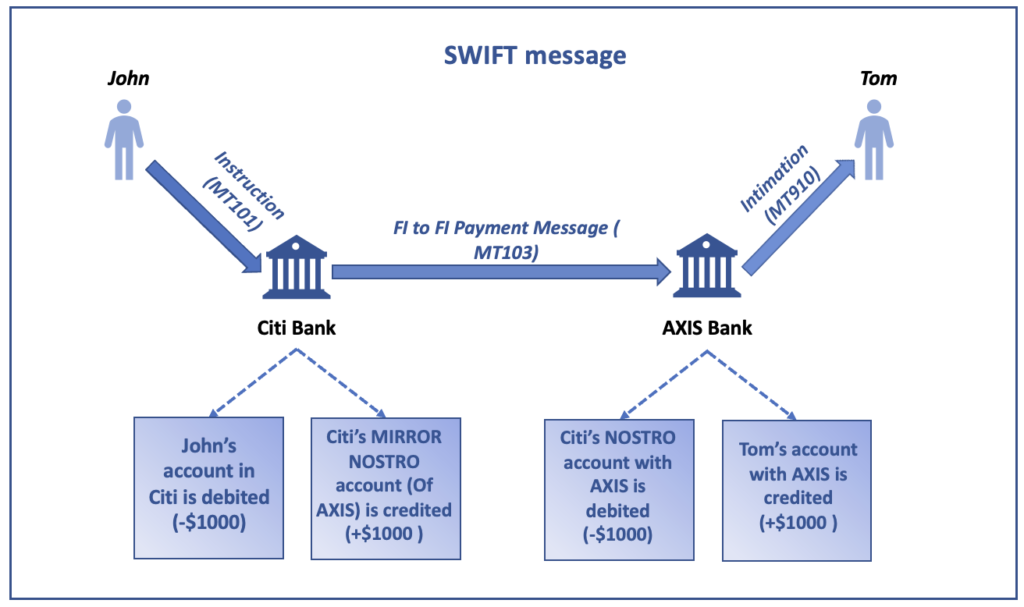

In this example, we will take a payment settle through correspondent banking

Step 1: John instructs his bank (Citi) to send funds ($1000) from his account to Tom’s account in AXIS bank via. the internet banking portal (Or any other channel). This instruction will be in the form of a SWIFT MT101 message. John does not create the MT101 but the IT system of the bank does.

Step 2: Citi bank will have a “payment engine” that will receive this instruction (MT101), perform a range of checks and if all the checks result in a positive outcome, then John’s account is debited $1000.

Step 3: Now the money taken from John’s account is credited into the Mirror of the NOSTRO account that Citi bank has with Axis. This is like handing over the money to AXIS bank.

Step 4: Now that the accounting entries within Citi bank are completed a payment message is sent by Citi bank to AXIS bank. This will be a SWIFT MT103 message.

Step 5: AXIS bank will have its payment engine and it will receive and process the MT103 sent by Citi. If all the checks are successful then Citi’s NOSTRO account is debited for $1000 and the same is credited to Tom’s account.

Step 6: Tom is intimated via email or SMS or credit advice that funds have reached his account. If Tom is a company then they might receive an MT910 ( Confirmation of credit).

If you do not understand SWIFT MT101, MT103 or MT910 then do not worry we will study them in detail during the next few articles.

At this point it is also worth remembering that for a bank to these SWIFT messages it must have something called an RMA with bank B.

RMA stands for Relationship Management Application. It was introduced by SWIFT to stop unwanted messages from reaching a bank that may put an additional burden on the operations teams. It’s a way to stop unwanted messages at the source i.e. the sender should have an RMA with the receiving bank in order to send SWIFT messages

In simple words, if bank A has an RMA with bank B then it means that bank A has a correspondent relationship with bank B.

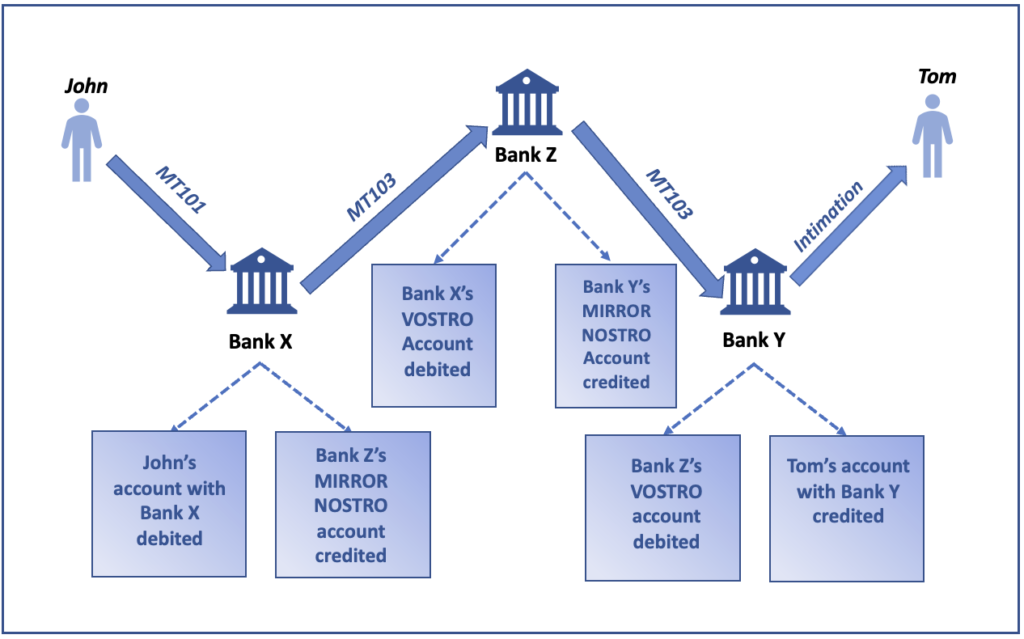

Let us now imagine that there are two banks bank X and bank Y, they are not part of a CSM aka PMI, they do not have accounts with each other (Nostro/Vostro) but they need to settle funds ie. Bank X’s customer has initiated a payment to bank Y’s customer. How is this possible?

Bank X and Y will find another bank with whom they both have an accounting relationship and correspondent relationship, and that bank Z can settle funds between bank X and Y.

Here you can see that Bank X sends an MT103 message to Bank Z and Bank Z forwards the MT103 to bank Y. This method of sending MT103 where each party forwards the MT103 to the next party in the chain is called the Serial method.

This method is often expensive as each party in the payment chain will add their charges. Banks X, Y, and Z will take their charges. It is also time-consuming.

Bank X decides to establish only a correspondent relationship with Bank Y so that it can send payment messages to Y but it will not be able to settle funds directly with Y as there is no accounting relationship.

Now, Bank X sends an Announcement to Bank Y that it will send the funds via bank Z and then Bank X also sends a Cover payment to Bank Z which carries the actual funds. This cover is then sent to Bank Y by bank Z.

Finally, when bank Y received both the announcement and the cover it reconciles (matches) both and credits the money to TOM. This is called the cover method. In certain cases, bank Y does not wait for the cover to arrive but directly processes the announcement. More about this later.

For now, don’t worry about the message types just try to follow the above explanation using the below Picture

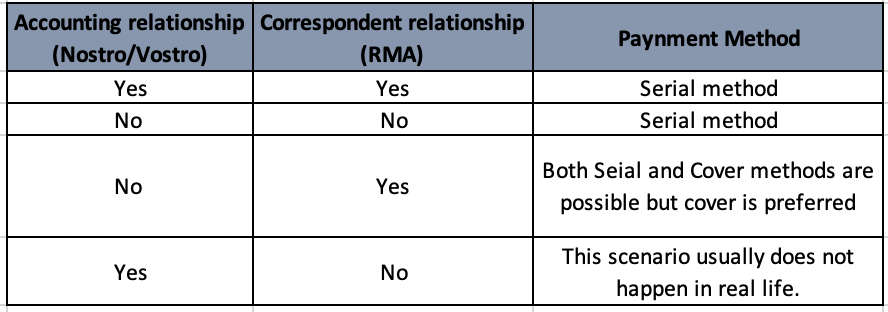

This table will help you understand when serial and cover messages are sent.

To summarize, here are the key differences between a serial and cover method

Leave a Comment

Learn Payments today from SharpTalents

About Me

Blog Comments

Rabi

November 21, 2021 at 10:37 am

Nicely explained.

Rohit Verma

November 23, 2021 at 2:08 pm

Thanks for explaining this…this has always been a bit confusing to most of the people 🙂

Deva Kumar

November 24, 2021 at 12:14 pm

Serial & Cover Methods Explained Beautifully!!!!!