Let’s Party

Nope!! These are not the parties you very much enjoy with your friends. These are the parties that act as pillars of the financial system.

We learned from the introduction that completing a single funds transfer involves several parties. The flow of information and funds happen from one party to another until the funds reach the account of the final beneficiary and he receives a satisfying “Your account has been credited with xxxxx” message. We, as the users of payment systems, might already be familiar with some of the obvious parties like Banks, Customers, etc. but there are also some not-so-obvious ones. This article (Hopefully) sheds light on the different parties in the chain.

Parties

- Customers

- Banks

- Clearing and Settlement Mechanism

- Third-Party Payment Solution Providers

- Governing Bodies

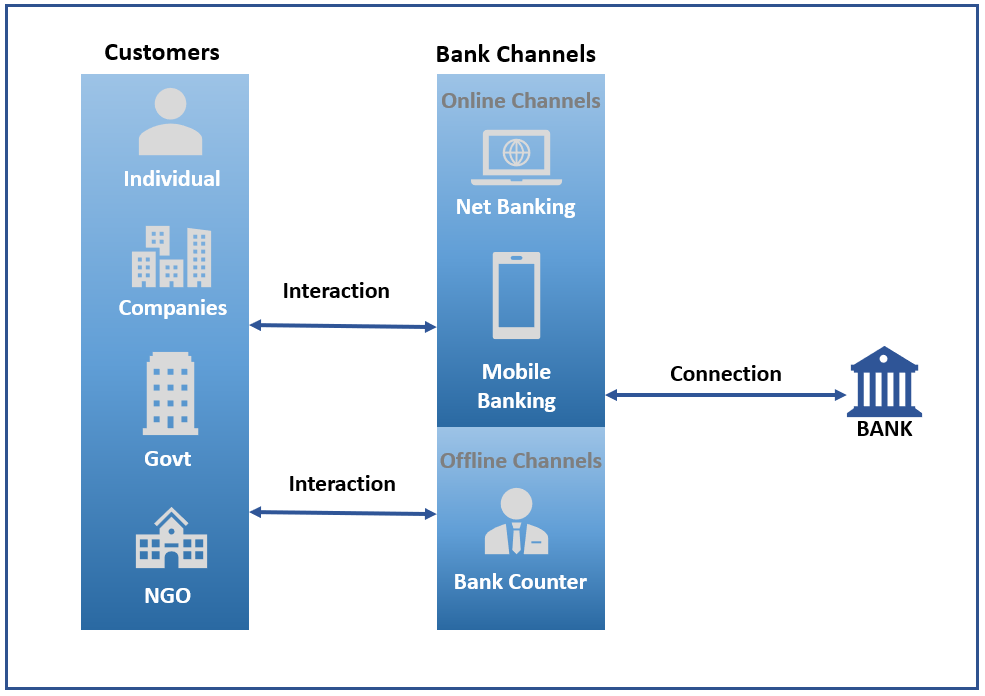

Customers

You might very understandably say “Really?!”, but the scope of this party is more than we think. Under the umbrella of the party ‘customer’, there are many entities and each of them has a variety of needs when it comes to funds transfer. These needs shape the solutions that banks/financial institutions provide.

A customer is any user who uses the bank’s solutions/product/facility to make fund transfers. A customer can be an Individual, Organizations, Companies (both big and small), branch of government, or NGO.

The role of a customer in the payment chain is usually as an initiator or a beneficiary of funds. The funds transfer where the end parties are customers of a bank has a separate category of their own. They are called customer credit transfers. Kindly take note of this phrase as most of our discussion will be on the same.

Customers generally use bank’s channels (Internet banking, Mobile banking, etc.) to initiate payments. The volume of fund transfers initiated by different types of customers widely vary. More about this topic (Transaction volumes) in future articles.

Banks

Banks are an important part of the payment chain. They act as facilitators and help their customers exchange funds. Banks benefit from this facilitation by charging their customers.

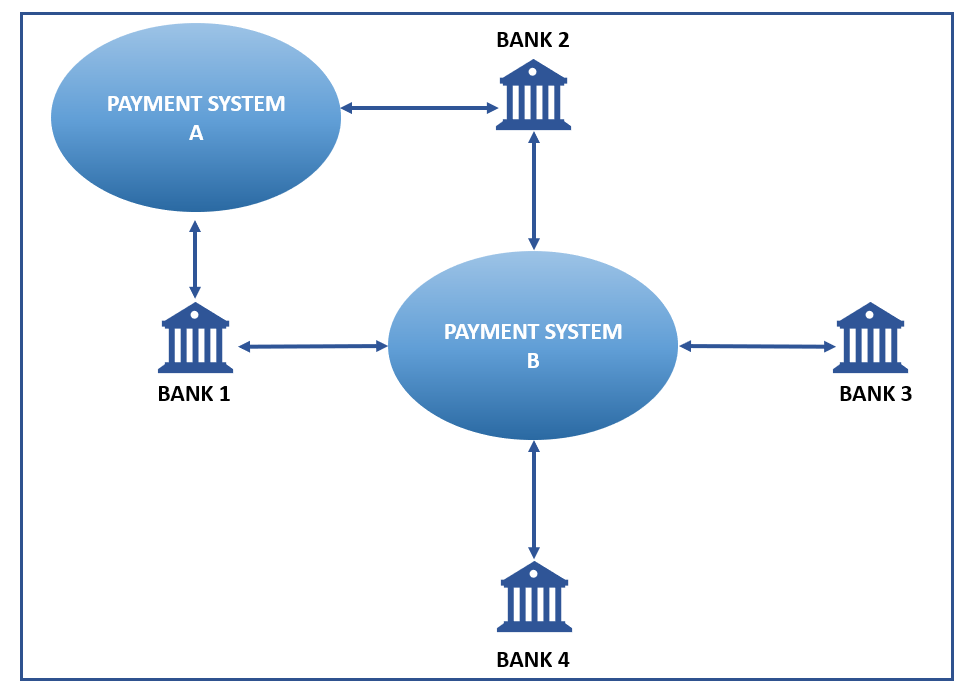

Banks also send funds to each other for various purposes like settlement, fee transfer, covering the funds of a customer transfer and so on.

It is important to understand that to exchange funds with one another, Banks should be part of a payment system. These systems are set up at the country level, region level, the international level. Each payment system has its own set of rules and regulations along with communication protocols. A bank may be part of one or more payment systems.

For example, a bank in Germany will be a direct participant of the SEPA payment system for exchanging funds within the EURO region and will be part of the cross-border payment system (SWIFT) for international fund transfers.

If you have questions about these payment systems, kindly note them down. For now, think of a payment system as network of banks who can exchange funds with each other.

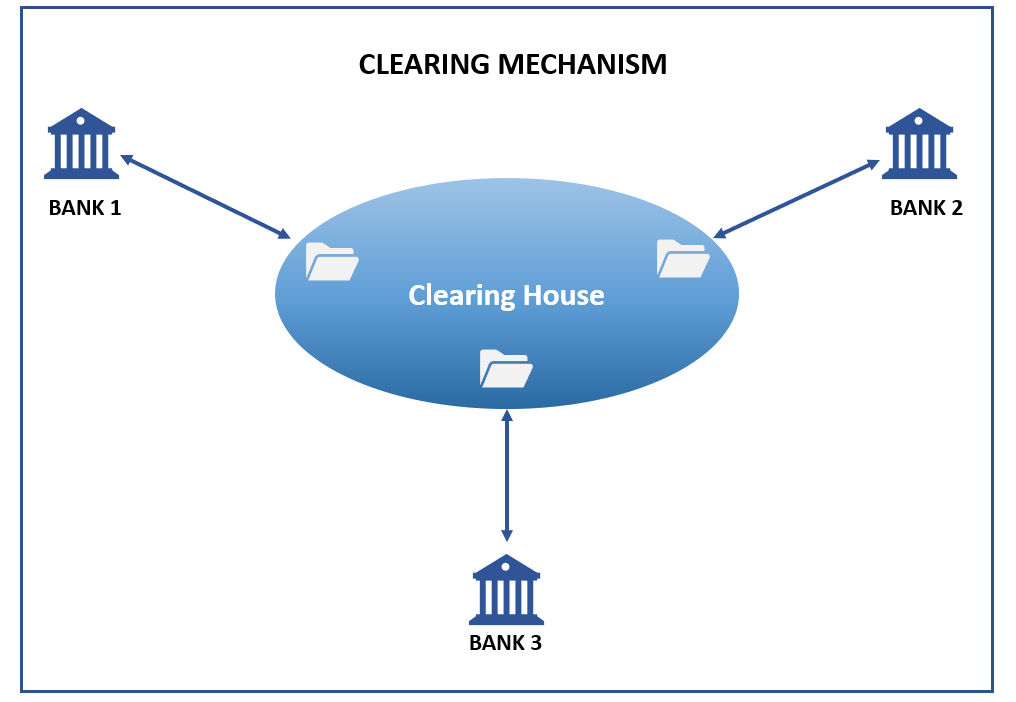

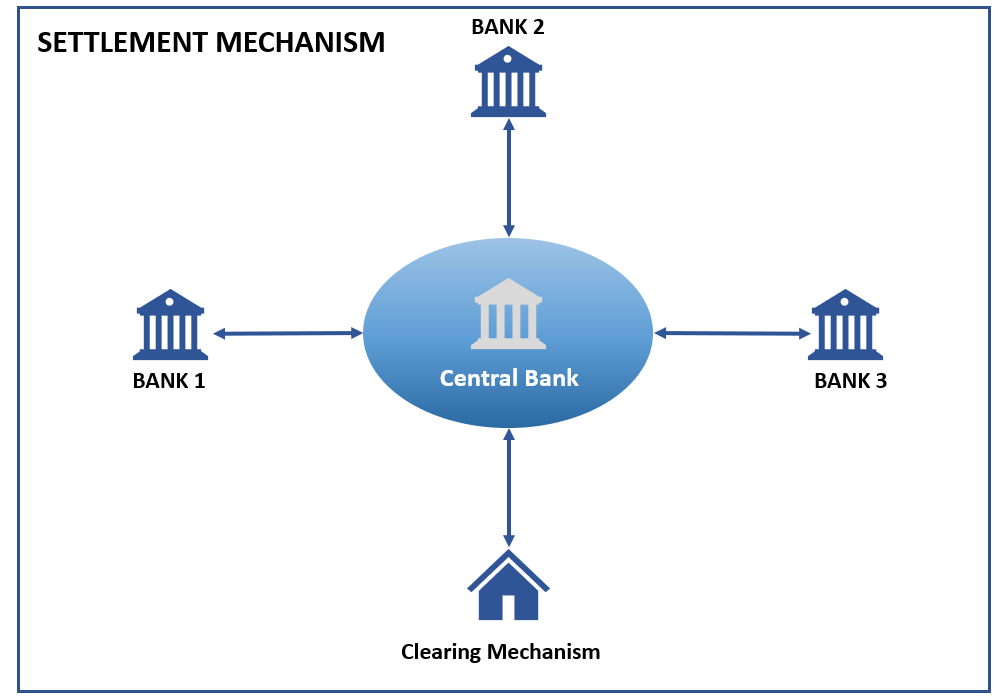

Clearing and Settlement Mechanism (CSM)

Any CSM performs two different tasks CLEARING and SETTLEMENT. The role of a CSM is to facilitate, regulate and simplify the exchange of funds between different banks.

In simple words, clearing is a process of validating payments and keeping track of how much a bank must pay other banks or how much other banks must pay them. Settlement is the process in which the actual movement of funds happen between banks. Settlement usually happens at the central bank level. Settlement may happen between two banks or between a clearing mechanism and banks.

Think of a clearing mechanism as a HUB that records and validates all the fund transfers among a group of banks. A company or an organization that does the clearing of payments is called a Clearing House. A couple of banks can do clearing among themselves (Bi-Lateral) or a group of banks may decide to form a clearinghouse and perform clearing (Multi-Lateral).

If you are still reading this article, then you deserve a huge pat on the back 😊 Keep reading there is a surprise as the end.

There are two types of settlements GROSS and NET. If the transactions are settled individually then it is GROSS settlement or if the final amount to be settled between banks is calculated (by clearing mechanism) and then the funds are exchanged, then it is called NET settlement.

Example of GROSS and NET settlement

Consider the following transactions,

Transaction number 1: Bank A sends Bank B $10 USD

Transaction number 2: Bank B sends Bank A $4 USD

If bank A settles 10 USD for transaction number 1 and banks B settles 4 USD for transaction number 2 then it is called GROSS settlement.

If Post completion of transactions 1 & 2, bank A settles only 6 USD (ie.10-4), then it is called NET settlement. This is how we settle money exchanges between friends in real life.

Memory Aid: Friends settlement = NET settlement

The clearing system calculates the NET settlement position of each bank once a day or several times a day and then settles the fund with the banks. There are certain systems like RTGS (Real-Time GROSS SETTLEMENT) that do not require clearing and settles funds among participants in real-time.

In short, CSM maintains the integrity of fund transfers and brings an overall trust factor to the payment chain. This is just an overview of CSM. If you wish to know more, kindly let me know in the comments section.

Third Party Payment Solution Providers

With the advent of open banking, banks are opening access to customer’s accounts by third parties with consent from customers. Customers can now use the solutions provided by these third parties to view their account balances and to initiate a funds transfer from their account.

These third-party providers (TPP) still use the traditional payment systems for fund transfers. It is important to take note of these TPPs as they are slowly changing the face of how we perform fund transfers. An example that I can give you is Google pay, yes the same google pay that paid you ₹ 800 for making a ₹ 30 transfer once 😊 .

Governing Bodies

These are the institutions the define the rules for exchanging funds with each other. They provide the necessary infrastructure and technology that makes digital payments a reality. They can be government bodies or private entities.

Let’s go lighter on this one. I will provide few examples and you can easily recognize who they are and what they do.

NPCI (National Payments Corporation of India)

EPC (European Payment Council)

SWIFT (Society for Worldwide Interbank Financial Telecommunication) – This abbreviation helped me land my first job in payments domain. Seriously !!, only this.

Now we come to the much-awaited surprise. “You are officially part of the payments domain”. If you had the patience to read the entire article, then you have a massive interest in payments. Interest is all it takes.

Leave a Comment

Learn Payments today from SharpTalents

About Me

Blog Comments

Sujamol J

May 15, 2021 at 5:31 am

Good Initiative Santosh. This is very helpful for clarity of perception in the field of requirement gathering.

Awaiting for your next topic.

Santosh

May 15, 2021 at 3:33 pm

Thank you

Hari Annamaraju

May 16, 2021 at 7:09 am

Very good information and consolidation of information in one place , thanks

Santosh

May 16, 2021 at 3:22 pm

Thank you

Srinivasan

May 17, 2021 at 8:00 am

Read the complete Article. Highly informative.

Thank you for your efforts.

Awaiting your further posts.

Santosh

May 17, 2021 at 3:45 pm

Thanks Srini

Shweta Verma

May 19, 2021 at 3:21 pm

This is really good.

I am really looking forward for more articles/blogs from you.

Thank you for putting efforts!

Dhanasudhan

May 20, 2021 at 8:29 am

HI Santosh please provide further information on CSM

Santosh

May 20, 2021 at 2:57 pm

May I know what type of info you are looking for ?? so that I can include it the next article.

Sai Laxman Morisetty

June 1, 2021 at 7:45 am

We got to know that Customers and banks communicate using payment messages. I want to know how does CSM communicates with Banks??

Santosh

June 1, 2021 at 8:04 am

Excellent question. I will write about it in the future articles.

Pratik

May 23, 2021 at 8:10 am

Nice article would like to understand more about commons functions performed at payment system like GPP, T24 etc

Santosh

May 25, 2021 at 7:20 am

Sure .. Thanks for your comments

Rama

May 23, 2021 at 3:21 pm

Gone through all the three articles. Very informative. Looking forward for upcoming articles

Santosh

May 25, 2021 at 7:18 am

Thank you

Birasing

May 24, 2021 at 9:59 am

Thanks,it’s nice

Santosh

May 25, 2021 at 7:15 am

Thank you

Vaibhav chawla

May 31, 2021 at 8:13 pm

Thank you for your efforts.

i have few queries :

a) Does a CSM will always be needed for a Fund transfer, if yes then it will be always central bank ?

b) Does A CSM is needed for domestic payments as well, lets say RTGS payments between two banks who does not have a nostro vostro relation with each other.

Santosh

June 1, 2021 at 8:09 am

CSM is not always needed. Clearing house can be a private company. Settlement between banks happens at the central bank level.

Domestic payments in most cases are done thorough CSM.

Accounting Entries in Payments – Payments Domain

June 4, 2021 at 5:09 am

[…] Parties in a Payment System […]

Dattatray Indore

June 4, 2021 at 6:20 pm

Great..I have experience in credit cards processing and wanted to learn about payments… really helpful… please guide to get opportunity to work and gain more knowledge in payments

Santosh

June 5, 2021 at 3:03 am

You can contact me via LinkedIn

Vinita Sarode

June 7, 2021 at 10:58 pm

Thank you

Shiva S

June 8, 2021 at 6:24 am

Hello Santhosh.

I really like the way you have presented the knowledge. Thank you so much for your efforts.

I have a question. Does the Clearing House have a Separate Software of its own? Or will the Clearing House be able to Interpret the Payment Message from the Banks?

Bank A – TEMENOS

CSM – Clearing House??

Bank B – BANCS

Santosh

June 8, 2021 at 2:52 pm

Clearing house will have software of its own .. Sometimes they get the software from Vendors.. Currently there a clearing called P27 that is being implemented in NORDICS which uses Volante

Ruchi Bajpai

November 10, 2021 at 6:42 pm

Hi Santosh!

Thanks for explaining everything in such a simple nd easy way..That’s what makes a difference.

.

Vishal Deshmukh

June 8, 2021 at 11:36 am

The way you explain about Gross and Net settlement now it’s really going easy for me understand regarding Settlement. Can you please cover topic about Reconciliation.

Santosh

June 8, 2021 at 2:49 pm

Sure

Shraddha

June 10, 2021 at 12:39 pm

Hi Santosh,

Thanks for your article !!

I have a query : SWIFT is a payment system or governing body?

Santosh

June 11, 2021 at 4:22 am

SWIFT as an organization will fall under the category of governing body.

PREMKUMAR A

June 11, 2021 at 6:28 am

Thank you for the article! Being a Fresher, these articles helped me a lot to grasp concepts better!

Vaibhav Agarwal

August 1, 2021 at 9:23 am

Have 6 years of extensive knowledge on Payments domain. But still am learning from these articles. Thanks a lot Santosh for these articles.

Santosh

August 1, 2021 at 11:55 am

I am really glad that it is helpful

Rahul

August 12, 2021 at 10:30 am

You articles are very easy to understand.

Can you explain below point:

In cover payment I know how initiator bank works and identify it is cover payment.

How about receiving bank, if a bank has received MT103, is there any check point which helps to determine that funds are going to come into receiving bank account as cover payment?

Santosh

August 14, 2021 at 6:03 am

Hello .. Yes.. If the fields 55, 54 and 53 are present then the MT103 will wait for cover

Rohit

August 15, 2021 at 11:15 am

Its really an amazing content for the payment begineers. Thanks a lot Santosh for explaining it a simple and lucid way.

Santosh

August 15, 2021 at 2:42 pm

Thank you so much

Deepakraj

September 1, 2021 at 10:19 am

Awesome Explanation ..Great work Buddy

Swati Dubey

September 25, 2021 at 9:44 am

Santosh , you should seriously publish your book.