PAYMENT MESSAGES

We might be getting ahead of ourselves here. There is a lot to understand about payments before we discuss messages, right?! I have a different view on this. My feeling is that payments could be better understood if we get our basics right about messages.

A common man might not have heard about payment messages at all. If you are from the IT/Software industry and have worked in banking, then you might have heard about them. In the real world, if not for the exchange of these messages, then the world’s economy would come to a halt.

What are these “messages” that I am talking about??

They are the carriers of payment information from one party to another. They start their journey from the ordering customer (Industry-standard term for a customer who initiated the payment) and ends with the Beneficiary Customer (Industry-standard term for a customer who receives this payment)

On a high level these messages are of two types:

- Customer to Bank / Bank to Customer (aka. Customer to FI / FI to customer)

- Bank to Bank (FI to FI)

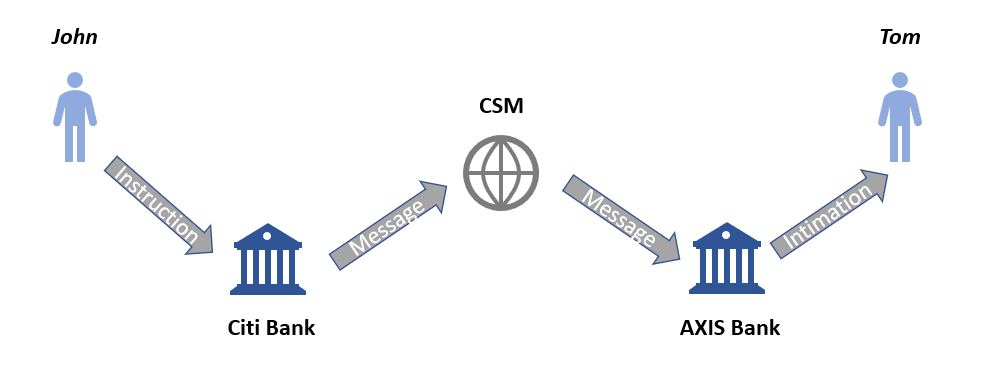

FI means financial institution. Do you remember the very first article?? Let us pull up the picture again for our reference.

Customer to Bank:

John does not personally type these payment messages. When he logs into the net banking portal he provides the details of the payment like the amount, currency, account number of the beneficiary, the bank’s code, and description of the payment, then the bank’s software converts it into a payment message.

This message is an instruction to the bank (Pic A0301) to initiate a credit transfer. A point to note here is that these ‘customers to bank’ instruction messages are not mandatory in most payment systems, but are recommended. Corporations send these types of payments directly to the bank.

These messages do not carry any funds in them but only instructions.

You may have a question here If these messages are not mandatory then in what other ways the instructions are passed to the bank. The answer to this is slightly technical. There are a variety of ways and it varies from bank to bank, but the most popular method used these days is API.

APIs are like waiters in a restaurant they take the order from one application (customer at a restaurant) to another (the kitchen).

Bank to Bank:

These are the messages that move funds from one bank to the other. In Pic A0301 they carry payment information and funds from Citi to Axis banks.

They are of two types

- Customer transfers

- Bank transfer

Confusion?? – Let me explain

Customer transfers: These are messages sent by one bank to another and at least one of the parties in the payment chain is a bank’s customer. The message sent by Citi Bank in pic A0301 is a customer transfer.

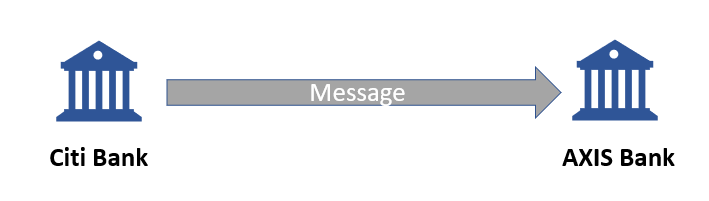

Bank transfers: These are messages sent by one bank to another and all the parties are banks. Banks send funds to other banks for reasons like fees, settlement amount, funding their accounts, etc. In the below picture(A0302) you can see a bank transfer message.

Bank to customer: These are mostly status messages or confirmations or advices related to funds transfer. The intimate the customer about the debit or credit of funds, statements, etc. . In most cases these are sent to corporate customers by the bank.

If you refer to my previous article Link, I had given a brief about the governing bodies. They actually decide the structure of these messages. Every year changes to these messages will be done based on the requirements of the market. These governing bodies also provide the secure infrastructure required for the transportation of these messages.

We still have not addressed the most important question. How is the actual money transferred from one bank to another?? Does a bank employee carry a suitcase full of cash to the other bank?? Definitely “No”

In My next article I will be talking about the accounting entries that happen in a transaction when these payment messages are sent and received.

Before we close, I want to talk about two more things.

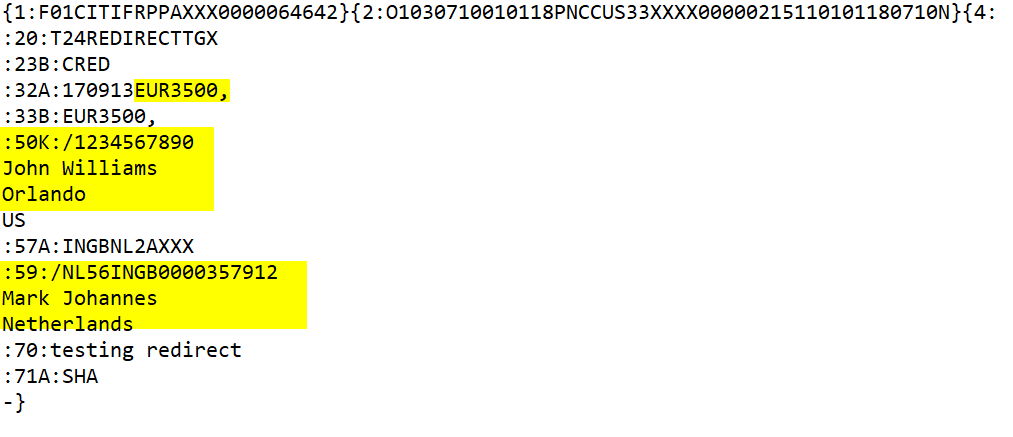

How does the ‘message’ actually look like??

If you are thinking that the messages are written in some sort of computer code then you will be quite surprised to learn that these messages are extremely readable. Below you can find the snippet of two of the most popular messages. We can easily take an educated guess on what the highlighted fields are.

SWIFT

SEPA

Quiz:

Here is a short quiz, you can email me the answer or message me in LinkedIn.

Beginner Level:

Name 3 examples of each of the different types of payments described above. You can of course use google, that is the whole point of it.

Professional Level:

Something in the swift message (Refer Pic A0303) is not correct. Can you identify it???

Leave a Comment

Learn Payments today from SharpTalents

About Me

Blog Comments

NAMISHA BATAR

May 23, 2021 at 8:47 am

Article is very helpful in understanding the basics of payments messages across different payment schemes as right now I am struggling a lot in getting to know direct debit.

Santosh

May 25, 2021 at 7:20 am

Thanks .. more coming soon

Chaitanya kumar g c

May 23, 2021 at 10:19 am

Different types of payments:

Customer payments:NEFT, RTGS, IMPS, SWIFT.

Bank to bank: Swift MT202, RTGS interbank.

Chaitanya kumar g c

May 23, 2021 at 10:22 am

Customer payments NEFT RTGS IMPS Swift

Bank to bank:RTGS, Swift MT 202.

Santosh

May 25, 2021 at 7:19 am

Can you name the payment message for customer payments .

Chaitanya kumar g c

May 28, 2021 at 2:50 pm

NEFT N06,RtGS Pacs 008,NACH Direct debit Pacs 003, Nach credit Pacs 008,IMPS ISO 8583 200

Kartik

May 30, 2021 at 5:42 pm

MT103 is used for customer to Bank and vice versa payment

Santosh

May 31, 2021 at 4:03 am

Actually MT103 is for Bank to Bank only with one of the end parties being a customer

Ravi

May 23, 2021 at 10:37 am

Maybe IBAN IN field 50?

Santosh

May 25, 2021 at 7:18 am

I am sorry .. I can give you a clue.. Nov 2020 SWIFT updates

Rachita

May 25, 2021 at 10:29 am

GPI missing

Santosh

May 28, 2021 at 3:26 am

Correct .. Actually a bank need not be a GPI member.. The exact term is universal confirmation

Saahil

May 23, 2021 at 3:37 pm

Nice articel !!

With refernece to your question regarding swift message , 3rd block is missing

Santosh

May 25, 2021 at 7:17 am

Thank you . Correct . I am looking for the specific tag 🙂

Manjiri

December 3, 2021 at 12:04 pm

block 3 – tag121: UETR

Santosh

December 9, 2021 at 4:47 pm

BINGO

Michael S

May 23, 2021 at 5:25 pm

Already messaged you on Linkedin. Just here to leave a message of support for the excellent insight you shedding using your blogging platform.

Keep up the good work!

Santosh

May 25, 2021 at 7:17 am

Thank you

Garima singh

May 23, 2021 at 6:26 pm

Types off SEPA payement messages

SEPA credit

SEPA direct debit

SEPA card

Type of Swift messages

Direct and indirect payment messages

Santosh

May 25, 2021 at 7:16 am

Can you mention the actual message names if possible ? 🙂

Rachita

May 25, 2021 at 10:29 am

GPI missing

Kartik Krishnamoorthy

May 30, 2021 at 5:47 pm

For individual customers->Bank MT103

For Bank to Bank MT202/210 is used based on the direction of the transaction.

SEPA (Single Euro Payment Area) is applicable to corporate banking – Had hands on around 6 years back.

Types:-

Single Credit Transfer

Bulk Credit transfer

Direct Debit

Bulk Direct Debit

Receivables

Santosh

May 31, 2021 at 4:02 am

You are right

Vaibhav chawla

May 31, 2021 at 8:45 pm

Ans 1 Block 3 tag 121 UETR and Tag111 GPI is missing

Ans2 Swift

Customer to FI MT101

Bank to bank MT202,MT103

Fi to customer MT 910,940

Sepa

Customer To Fi pain.001

Bank to Bank pacs.009,Pacs.008

Fi to customer Camt 52

Thanks

Vaibhav chawla

May 31, 2021 at 8:46 pm

Ans 1 Block 3 tag 121 UETR and Tag111 GPI is missing

Ans2 Swift

Customer to FI MT101

Bank to bank MT202,MT103

Fi to customer MT 910,940

Sepa

Customer To Fi pain.001

Bank to Bank pacs.009,Pacs.008

Fi to customer Camt 52

Thank you

Santosh

June 1, 2021 at 8:05 am

Awesome Vaibhav . 111 is not mandatory if the bank is not a GPI member.

Vaibhav chawla

June 1, 2021 at 1:25 pm

Yes that’s right.

Thank you

Shiva S

June 8, 2021 at 7:04 am

Sharing few Standard types of SWIFT Message Types. Based on Google.

MT 103

MT 202

MT 900

Santosh

June 8, 2021 at 2:49 pm

Great 🙂

Shiva S

June 8, 2021 at 7:18 am

Sharing few Message Types for SEPA Payment Engine. With help from Google. 🙂

Pain.001

Pain.002

Pacs.003

Santosh

June 8, 2021 at 2:49 pm

Great 🙂

Sreeya

June 28, 2021 at 3:12 pm

Hey Santosh,

Great narration as always. More power to people who choose to spend time in sharing their knowledge.

Just one observation regarding the section you introduced about payment messages – “and ends with the Beneficiary Customer (Industry-standard term for a customer who receives this payment” – may not be always the case as in case of Pull transactions the message and cash flow in opposite directions. But yes, the message always starts from the initiator of the payment, be it the payer or the beneficiary.

Santosh

June 28, 2021 at 4:19 pm

In a credit transfer (Push payment), the initiating party is the ordering customer and the payment ends with the beneficiary customer. Here the beneficiary does not initiate the payment. In a Direct debit transaction (Pull Payment), the beneficiary initiates the transaction but the payment still ends with the ben customer. So far I have not introduced direct debits and the examples in the current article are wrt of credit transfers only. When we talk about DDs in the future I will explain how it is different from a CT. Glad that you brought this up. If someone has a query on this the comments section will clarify their doubts.

Rajesh Pujapanda

December 3, 2021 at 11:37 am

Beginner Level answer:

MT103, MT202, MT101, MT940

Professional Level answer:

TRCKCHZZ is missing